By: Katelyn O’Dell Dean and Zahava Urecki, Bipartisan Policy Center

Overview

The Department of Energy (DOE) office responsible for administering loans and loan guarantees—formerly known as the Loan Programs Office (LPO) and recently renamed the Office of Energy Dominance Financing (EDF)—is one of the federal government’s most valuable tools to advance end-to-end American energy innovation. DOE’s loan programs not only strengthen U.S. energy and national security but also help keep energy prices low and the U.S. energy sector globally competitive. Through low-interest direct loans and loan guarantees,[1] DOE can accelerate the pace of innovation by bridging the gap between technologies that have been proven at pilot-scale and overcoming impediments to deploying on a commercial scale. Since their beginnings in the Energy Policy Act of 2005, DOE’s loan programs have received strong bipartisan support. They have also faced criticism over the failures of several high-profile projects. Unfortunately, these failures have created a risk-averse culture within DOE. Further, a lengthy application and loan closing process has persisted, presenting a barrier for many potential projects.

Recent congressional legislation has created the opportunity to consider new approaches to shaping the program portfolio and improving program execution. The 2021 Bipartisan Infrastructure Law (BIL) and the 2022 Inflation Reduction Act (IRA) expanded DOE’s loan guarantee authorities to include already-proven commercial decarbonization technologies and projects. The 2025 One Big Beautiful Bill Act (OBBBA) expanded the scope of eligible commercial technologies and limited the focus on reducing greenhouse gas emissions. OBBBA also significantly rolled back direct federal spending on energy technology innovation across the research, development, and demonstration (RD&D) spectrum. The net effect of these major statutory changes is to place increased emphasis on the role of DOE’s loan programs in federal energy innovation policy, prompting the need to reassess the Office of Energy Dominance Financing and its project portfolio and program execution strategies.

In October 2025, the Bipartisan Policy Center and the EFI Foundation (EFIF) organized a discussion among experts actively working on ways to cost-effectively leverage DOE’s loan program authority to foster energy innovation while benefiting the U.S. economy. From this discussion, three possible strategies for EDF to more effectively execute its mission emerged:

- Shift to a portfolio-based risk management approach with increased diversity in acceptable risk of the projects within the portfolio.

- Increase coordination among federal government activities to enhance risk management of the EDF portfolio.

- Increase the efficiency of the application and loan closure process with revised credit subsidy calculations and innovative lending structures.

In the following sections, we provide details about these proposed strategies, including the problems they may solve and the opportunities they could create. Although these strategies are neither comprehensive nor the ultimate path forward for EDF, we hope they will serve as a catalyst for ongoing dialogue to maximize EDF’s potential to support America’s energy future.

20 Years of DOE’s Loan Programs

The 2005 Energy Policy Act gave DOE the authority to provide affordable debt financing for innovative clean energy technologies that are technologically proven but not yet widely deployed. DOE’s loan programs began with two distinct authorities:

- The Title 17 Clean Energy Financing Loan Guarantee Program, which supports projects that reduce emissions with innovative technologies.

- The Tribal Energy Loan Guarantee Program, which supports energy projects owned by a tribal government or tribal development organization.

The mission of Title 17, as set forth in the statute, is to “employ new or significantly improved technologies as compared to commercial technologies in service in the United States.” DOE’s debt financing authorities were expanded through the creation of the Advanced Technology Vehicles Manufacturing Loan Program (ATVM) in the Energy Independence and Security Act of 2007. The law authorized DOE to issue direct loans to automobile manufacturers and component suppliers for light-duty vehicles and qualifying components that use advanced technology. The statute defined qualifying vehicle technologies and components as those which provide either a reduction in emissions or increases in fuel economy.

Over the past 20 years, DOE’s loan programs have played pivotal roles in providing early debt financing for major energy and vehicle technology innovations. For example, the Energy Department supplied a loan guarantee of $456 million to finance Tesla’s first large-scale factory in 2010, as well as a total of $4.6 billion to help finance the first five photovoltaic solar projects larger than 100 megawatts beginning in 2011. Since 2014, DOE has provided loan guarantees totaling $12 billion to finance the first new gigawatt-scale nuclear reactors in the United States in over three decades. However, as with any lender financing innovative projects, DOE’s loan program portfolio has not been without losses. The Energy Department has faced criticism over the years when a high-profile project, such as the Solyndra solar technology project in 2011, failed. Nonetheless the department’s successes have far outweighed its failures in terms of overall loan loss rate, which currently sits at around 2%, nearly matching the loan loss rate for commercial bank lending to projects that pose much less technology risk.[2]

The 2021 BIL expanded the eligibility criteria for existing DOE loan programs and created the Carbon Dioxide Transportation Infrastructure Finance and Innovation Program. Specifically, the legislation expanded ATVM program eligibility to include medium- and heavy-duty vehicles, aviation, hyperloop transportation, locomotives, and maritime vessels. The BIL also expanded eligibility for the Clean Energy Financing Program (also known as 1703) to include critical minerals processing, manufacturing, and recycling, and the legislation removed the innovation requirement for State Energy Financing Institution projects.[3]

The 2025 OBBBA repealed over $8 billion in IRA appropriations for credit subsidies across DOE loan programs, increasing upfront costs for applicants. However, DOE’s authority under the Energy Infrastructure Reinvestment (1706) Program also saw major expansions in program eligibility in OBBBA to include critical minerals projects, reinvestment in all forms of energy infrastructure, and new electricity generation projects for maintaining grid reliability or improving other system needs. OBBBA also appropriated an additional $1 billion in credit subsidy funds for this purpose in the newly modified and expanded 1706 program, which was renamed Energy Dominance Financing Program (EDFP).

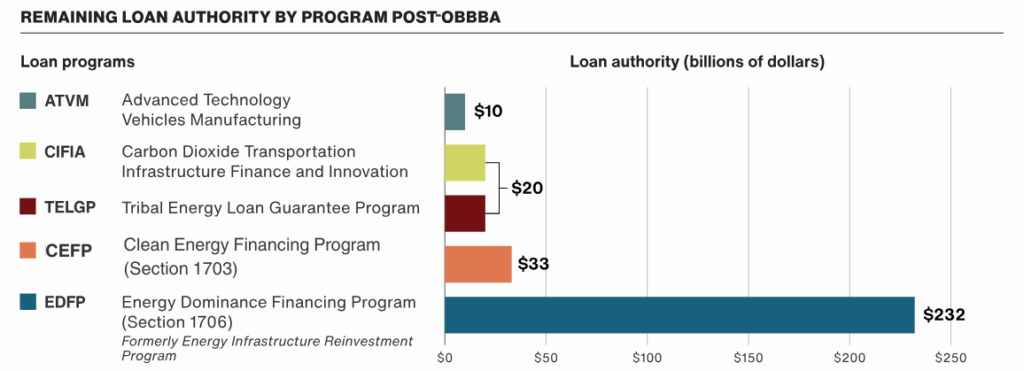

Today, the Energy Department’s EDF maintains five distinct programs with over $300 billion in loan authority (Figure 1).[4] According to current estimates, available credit subsidy across EDFP, ATVM, and the Clean Energy Financing Program sits at just under $4 billion.[5] Remaining unobligated credit subsidy is concentrated in the ATVM. Since the issuance of the first loan guarantee, DOE has issued over $130 billion in loans or loan guarantees for nearly 100 project locations. Currently, there are 46 active loans and 25 conditional commitments, totaling $118 billion. In just the last two months, DOE has finalized three loan guarantees for rebuilding transmission lines, enabling coal-powered fertilizer production, and restarting the former Three Mile Island nuclear power plant.

FIGURE 1. Status of DOE Loan Authority by Program after OBBBA[6]

Source: 2025 EFIF Report: DOE Staff Crunch Slows American Energy Innovation

The recent legislation and changes in project activity indicate a continuing strong bipartisan interest in expanding the role of the Office of Energy Dominance Financing, with EDF being seen as a powerful tool to advance energy technologies. Given this interest, BPC and EFIF convened loan program experts in October to discuss the program’s future and develop strategies for maximizing the program’s potential. The discussion covered three themes:

- Defining current opportunities for the loan programs to “meet the moment” and support energy technologies aligned with the administration’s priorities.

- Aligning on the most critical new and ongoing challenges that need to be addressed to ensure that DOE’s loan programs remain able to effectively execute on the office’s mission and to identify strategies to address these challenges.

- Sharing views on the overall direction of the loan programs and how they can be best leveraged to meet the nation’s energy needs now and in the future.

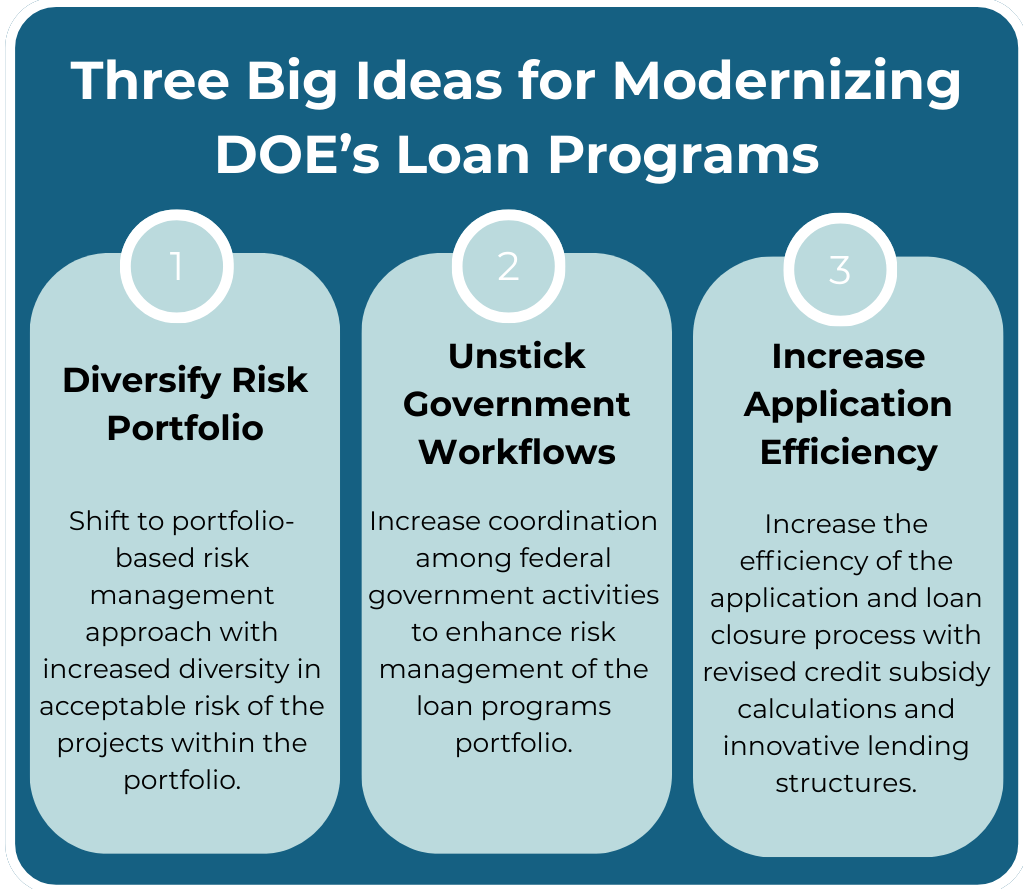

Three Big Ideas for Modernizing DOE’s Loan Program

FIGURE 2. Three Big Ideas for Modernizing DOE’s Loan Programs, as Identified by Workshop Participants

Source: EFI Foundation

1. Diversify Risk Portfolio

EDF should consider shifting to a portfolio-based risk management approach with increased diversity in acceptable risk of the projects within the portfolio.

DOE’s loan program has a history of unclear parameters for risk tolerance that has often been misaligned with its initial statutory purpose: to provide financing for projects that could not otherwise access affordable debt financing to cross the “valley of death” between demonstration scale success and broad commercial deployment. DOE’s lifetime loan loss rate sits at approximately 2%, which is near the level of most commercial banks (1.3%).[7],[8] However, the DOE was never intended to operate as a commercial bank; Congress wanted the Energy Department to develop next-generation energy technology to enhance U.S. competitiveness by providing financing to projects that were not yet at commercial scale and thus could not get affordable loans from commercial lenders. When DOE operates within the narrow risk tolerance level of a commercial bank, it is duplicating commercial activities rather than focusing on its original mission of filling the financing gap facing early-stage innovative technology projects. DOE should consider developing a strategic and diverse risk profile across its entire loan portfolio that better reflects the market readiness of eligible projects within each program.

Inherent risk-aversion has persisted throughout the history of DOE’s loan programs and across multiple administrations of both political parties due to the high-profile nature of many of the program’s projects.[9] DOE has selected and closed deals with projects based on their individual upside potential and risk, and the program has subsequently been defined by the successes and failures of individual projects. Persistent criticism of the loan office and its staff after failed projects has led DOE to conduct overly extensive and conservative diligence processes with new projects. Without a portfolio-wide risk management strategy, accompanied by a clear strategic communications plan, the EDF’s portfolio risk will remain too conservative to fulfill the federal government’s role in bringing innovative technologies to market.

Workshop participants highlighted several key ways to foster a more strategic risk management strategy, including:

- Define a range of acceptable risk tolerance at the portfolio level with bounds on acceptable risk that vary across the loan programs and reflect their eligible technologies, market maturity, and overall mission.

- Consider setting clear, targeted program-level or subprogram level risk management goals (e.g., industry-specific or technology-specific) to increase the diversity of projects chosen and improve public communication of the purposes, priorities, and risk profiles of the EDF programs.

Clearly defined portfolio-based risk targets and goals across multiple projects will reduce the conservatism of project-by-project decision-making. This, in turn, will empower EDF to accelerate the pace of energy innovation by increasing the diversity of projects and technologies. Providing reasonable guardrails on acceptable loan loss rates or target return rates could help guide EDF staff to accept levels of risk more in line with the original intent of the program and its authorities. A portfolio risk management approach could also allow EDF to define different levels of risk tolerance for certain authorities or program areas where a certain risk tolerance may be desired, more politically feasible, or required to meet program goals.

Improving messaging around the performance of DOE’s loan portfolio to Congress and the public is essential to maintaining an ability to take the level of risk required to advance innovative technologies. A portfolio-wide risk management strategy could allow the office to redefine the program’s performance broadly across the portfolio or authorities, thereby not allowing a single project to define success or failure for the program.

2. Unstick Government Workflows

DOE should consider increasing coordination among federal government activities to enhance risk management of the loan programs portfolio.

Large infrastructure projects require interaction with multiple federal agencies to receive permits, complete environmental reviews, and comply with relevant regulations. Although not a problem unique to DOE and EDF, a lack of coordination across the federal government can increase risks for EDF projects. Better coordination could streamline multiagency reviews and help accelerate project timelines while reducing external risk within the government’s control.

DOE’s loan programs have historically operated on a stand-alone basis, without the benefit of full government integration. Operating in a silo can increase risk that could be better managed through integration of federal efforts. Infrastructure projects, especially for emerging technologies, are often decades long and require different capital structures for each phase of the project. A single project may require grant-style funding during the early development phases and low-interest loans for a later construction phase. Moreover, demand-side support, such as direct or indirect procurement policies, can bolster offtake certainty for emerging technologies and products. A lack of coordination among DOE offices along the research, development, demonstration, and deployment (RDD&D) pipeline, along with heavy restrictions on interactions of different types of federal support across federal agencies, can place increased risk on EDF-supported technologies and projects. These obstacles can even prevent good candidates from applying for support from DOE loan programs.

Workshop participants identified three strategies to enhance government coordination involving DOE loan program projects:

- Facilitate agency cooperation by designating “quarterbacks” to lead top-down multiagency reviews of projects, which will reduce external project risk within the government’s control.

- Strengthen DOE’s agency-wide approach to energy technology commercialization to ensure smooth transitions across the RDD&D pipeline by instituting centralized cross-office coordination.

- Reduce support restrictions that prohibit projects from receiving a loan or loan guarantee if it previously received other supply-side or demand-side federal support.

Designating senior-level quarterbacks for multiagency reviews of DOE’s loans and loan guarantees, or instituting a fast-track process for permitting, can increase coordination among agencies. These strategies could be deployed within the National Energy Dominance Council, established by President Donald Trump earlier this year, or the Federal Permitting Improvement Steering Council, which was recently leveraged to streamline federal permitting for data centers.[10]

Coordination among DOE offices is needed to bridge the demonstration gap along DOE’s RDD&D pipeline for innovative energy technologies. Bringing innovative technologies to market relies not only on DOE loans but also on grants, demand-side support, and other transaction agreements issued by other DOE offices and other federal agencies. Reducing federal support restrictions could help foster an agency-wide approach to energy innovation, allowing for coordinated federal participation across the long life and diverse capital stacks of commercial scale projects.

3. Increase Application Efficiency

DOE should consider increasing the efficiency of the application and loan closure process with revised credit subsidy calculations and innovative lending structures.

The elaborate loan and loan guarantee application process has led to long, unclear review processes, hindering projects’ potential for success before they even begin. Additionally, costs associated with DOE loans and loan guarantees rely on case-by-case, time-intensive credit subsidy calculations managed by the Office of Management and Budget (OMB) that are highly conservative and may not reflect actual performance of the EDF program portfolio in more recent years.

Workshop participants identified two main areas for increasing the efficiency of EDF applications and loan closure process awards:

- Revise OMB’s credit subsidy calculation model to better reflect EDF’s historical performance and loss rates.

- Optimize underwriting processes by setting credit subsidies through broader risk-based categories and providing incentives for successful projects to exit the program.

Revising OMB’s credit subsidy calculation model and streamlining the underwriting processes where appropriate could save EDF both time and taxpayer dollars in the loan closure process. Creating a credit subsidy calculation model that appropriately reflects DOE’s historical performance and loss rates across the loan portfolio could reduce credit subsidy costs to both DOE and private-sector partners. Some participants suggested that EDF should also consider using DOE’s other transaction authority to lighten the heavy paperwork and requirement burden associated with its current application and loan closure process. Finally, if a project is successful, adding some type of incentive to exit the program (i.e., an option to refinance and exit EDF early, putting more money back into EDF’s program) could streamline the underwriting process, enabling EDF to issue loans and loan guarantees at a more appropriate pace.

Calculating credit subsidies by predetermined risk categories or profiles, instead of calculating at the individual project level, could optimize the loan closure process and enable a less time-intensive application process. Using standardized risk bands could allow DOE and OMB to apply consistent assumptions across similar technologies, reducing the need for bespoke modeling and repeated negotiations for each applicant. It could also provide clearer market signals by aligning subsidy levels with transparent, portfolio-based risk groupings, helping developers to better anticipate financing terms and to structure their capital stacks earlier in the process.

Conclusion

The strategies to modernize DOE’s loan programs outlined in this paper stem from a dialogue among DOE loan program experts convened by BPC and EFIF and reflect a shared vision to maximize the program’s potential to bring promising technologies to market. Although these recommendations lay a strong foundation for reform, they are not exhaustive. Rather, they represent an initial step toward a broader conversation about the future of DOE’s loan programs and how they can maintain their position as some of the federal government’s most effective tools for advancing end-to-end American energy innovation.

Learn how we’re tracking implementation at the DOE:

Explore the Energy Innovation Project

[1] Loans refer to direct loans approved by DOE and disbursed by the Treasury Department to the borrowing entity. DOE issues loan guarantees to borrowers to guarantee DOE repayment of these commercial loans. The borrower relying on DOE loan guarantees also becomes eligible to borrow from the Federal Financing Bank, a separate arm of the Treasury.

[2] U.S. Department of Energy. EDF portfolio performance. U.S. Department of Energy. Retrieved December 11, 2025, from https://www.energy.gov/edf/edf-portfolio-performance

[3] U.S. Department of Energy, Loan Programs Office. Inflation Reduction Act of 2022. U.S. Department of Energy. Retrieved December 11, 2025, from https://www.energy.gov/lpo/inflation-reduction-act-2022

[4] In addition to the legislative authority to issue loans or loan guarantees within a specified authorization cap, the 1990 Federal Credit Reform Act requires that the credit subsidy of the loan or loan guarantee agreement be recorded in the budget as an obligation and outlay. The credit subsidy is the net present value of the probability of a future default on repayment of the loan (adjusted for any estimated recovery value from the disposition of the project). The credit subsidy is paid at the time of the closing of the loan agreement, either with a federal appropriation earmarked for this purpose or as a fee paid by the borrower. OBBBA rescinded the unused balances of credit subsidy appropriations for a number of EDF programs, with a new appropriation of $1 billion of credit subsidy for the restructured Energy Dominance loan guarantee program.

[5] Hochman, T. (2025, July 18). What happened to LPO? Green Tape. https://www.greentape.pub/p/what-happened-to-lpo

[6] DOE’s ability to issue loans also relies on the available credit subsidy. At the time of loan closure, credit subsidies must be paid either by the borrower or the federal government with appropriated credit subsidy funds.

[7] U.S. Department of Energy. EDF portfolio performance. U.S. Department of Energy. Retrieved December 11, 2025, from https://www.energy.gov/edf/edf-portfolio-performance

[8] Board of Governors of the Federal Reserve System. Delinquency rate on business loans, all commercial banks (DRBLACBN) [Data set]. Federal Reserve Bank of St. Louis. Retrieved December 11, 2025, from https://fred.stlouisfed.org/series/DRBLACBN

[9] In the early days of LPO, the Congressional Budget Office (CBO) arbitrarily assigned an additional default score of 1% to LPO loan authorities on the presumption that DOE would systematically underestimate the risk of all projects in the portfolio. This caused LPO to take an overly conservative approach to risk. The George W. Bush administration subsequently was able to persuade CBO to drop the 1% across-the-board risk penalty.

[10] The White House. (2025, July 23). Executive Order 14318: Accelerating Federal Permitting of Data Center Infrastructure. Federal Register.